Singlife Savvy Invest is an investment-based ILP with one of the lowest fees in the market (and easily one of the best)

This is Singlife’s first venture into the ILP business, and it seems pretty good to us!

Here’s our review of the Singlife Savvy Invest:

My Review of the Singlife Savvy Invest

The Singlife Savvy Invest is an excellent policy that offers the freedom to manage your investment to meet your needs.

With this plan, you can make single premium top-ups, partially withdraw your funds, or change the funds to meet your needs.

Since the fees are comparable with Manulife InvestReady Wealth II, we compare them against each other.

| Singlife Savvy Invest | Manulife InvestReady Wealth II | |

| Charges | Administrative and supplementary charges are 0.65% and 1.85% p.a respectively | Administrative and supplementary charges are 0.7% p.a and 1.80% respectively |

| Optional Riders | Payer Premium Waiver Benefit and Payer Critical Illness Premium Waiver II | Optional early critical illnesses waiver coverage, cancer waiver coverage, or Payor benefit. |

| Fund Offerings | About 100 | About 140 |

| Bonuses Available | Welcome and Loyalty | Welcome, Loyalty, and Renewal Bonus |

| Premium Payment Terms | 3, 5, 10 years fixed

5, 10, 20 years flexible |

3, 5, 10 years fixed

3, 10, 20 years flexible |

When you compare it with the Manulife InvestReady Wealth II, the Singlife Savvy Invest is more affordable – 0.05% per year, after the first 10 years, to be exact.

Putting both under the same conditions for the above illustration, Singlife Savvy Invest brings in $2,498.73 more for you after 30 years.

However, this excludes the bonuses from both ILPs.

When looking at the bonuses, there are slight differences, but both will provide you similar bonuses of up to 60% depending on your MIP and investment amount.

However, only Manulife’s InvestReady Wealth II provides a Renewal Bonus. This goes up to 20% of your account value at the point of policy renewal – giving you a huge boost to compete against the 0.05% difference.

It’s worth noting that the Singlife Savvy Invest has a Loyalty Bonus that’s 0.2% higher than Manulife’s.

So in terms of affordability, I’d say they are on par with each other. It really depends on the MIP you’ve chosen, the investment amount, and your time horizon.

Next, we talk about potential returns.

The Singlife Savvy Invest has access to accredited investor funds, which gives you much higher returns than funds retail investors like us can get.

So this means the potential returns on the Savvy Invest, by theory, are much higher than the Manulife InvestReady Wealth II.

But this really depends on how well your financial advisor manages your portfolio – you can get access to the best funds, but if it’s not well managed, you’d get bad returns too.

And not forgetting that AI funds mean higher charges for your unit trust, and more risks taken.

Like any ILP, Singlife Savvy Invest offers a long-term option to accumulate your money to cushion you during your golden years.

To decide on whether you should get Singlife Savvy Invest depends on the circumstances you’re in and the type of individual you are.

After all, no single ILP is 100% excellent.

We recommend starting by reading our post on the best ILPs in Singapore – giving you an understanding of your choices.

From there, you should get a second opinion from an unbiased financial advisor on whether the Singlife Savvy Invest is the best policy for you.

Just because we like it and think it’s one of the best means it suits you too!

And if you’re about to invest $200 for the next 20 years, you should definitely take some time to make sure you’re making the right decision.

If you’d like to get a second opinion, we partner with MAS-licensed financial advisors who have helped thousands of our readers in this exact same situation.

If this interests you, click here for a free non-obligatory second opinion.

Now let’s explore in detail what the Singlife Savvy Invest has to offer:

Criteria

The minimum and maximum entry ages depend on whether you choose fixed or flexible premium payments.

Here is a summary of the entry requirements.

| Minimum Investment Period (MIP) | 3-Years Fixed | 5-Years Fixed | 5-Years Flexible | 10-Years Fixed | 10-Years Flexible | 20-Years Flexible |

| Minimum Age | 1 | |||||

| Maximum Entry Age | 65 | 65 | 65 | 60 | 60 | 60 |

When applying for a newborn baby you must be at least 30 years of age.

General Features and Benefits

Premium Payment Terms

You can choose the minimum investment period (MIP), either flexible or fixed, for a duration of 3, 5, 10, or 20 years.

Additionally, you can choose the premium amount you want to invest (starts at $200).

Here is an illustration of the regular premium per investment period.

| MIP | 3-Years Fixed | 5-Years Fixed | 5-Years Flexible | 10-Years Fixed | 10-Years Flexible | 20-Years Flexible |

| Monthly | 834 | 834 | 1,000 | 300 | 500 | 200 |

| Quarterly | 2,500 | 2,500 | 3,000 | 900 | 1,500 | 600 |

| Semi-annually | 5,000 | 5,000 | 6,000 | 1,800 | 3,000 | 1,200 |

| Yearly | 10,000 | 10,000 | 12,000 | 3,600 | 6,000 | 2,400 |

Note that all figures in the table are in SGD.

Premium Allocation

The policy invests all your premiums into an ILP sub-fund that you choose.

Minimum Investment Options

The plan has 2 different options for its minimum investment as highlighted below;

- Fixed

- Flexible

Each option provides you with varying periods that you can choose depending on your needs.

Here is a table to illustrate.

| Options Available | Fixed | Flexible |

| Minimum Period | 3 Years | 5 Years |

| 5 Years | 10 Years | |

| 10 Years | 20 Years |

Worth noting you can only choose the minimum period during application. After that, it’s not possible to change once the policy is accepted. However, you can adjust the premiums after the fixed term.

For flexible terms, the policy sets the limits such that you don’t have to wait for the expiry of the minimum investment period to change the basic regular premium.

Here is a table to illustrate.

| MIP | When you can change the basic regular premium |

| Fixed 3 Years | From the 4th year |

| Fixed 5 years | From the 6th year |

| Fixed 10 years | From the 11th year |

| Flexible 5 years | From the 4th year |

| Flexible 10 Years | From the 4th year |

| Flexible 20 Years | From the 11th year |

The minimum investment period starts from the policy effective date. The following charges will apply in certain situations.

| Charge | Circumstance |

| Premium shortfall charge | If you miss paying the basic regular premium |

| Partial withdrawal charge | If you make a partial withdrawal from the policy except under Life Stage Benefit |

| Surrender charge | If you surrender the policy in totality |

Difference between Fixed and Flexible Minimum Investment Period

The table below summarises the differences between Fixed and Flexible MIP.

| MIP | Fixed | Flexible |

| Basic regular premium threshold | A lower amount is needed | A higher amount is needed |

| Flexibility of the premium | Basic regular premium cannot be changed throughout the investment period | You can change the basic regular premium throughout the investment period depending on the available limits |

| Welcome bonus | Higher bonus for signing up | Lower bonus for signing up |

| Premium shortfall fee | I) Applies during the minimum investment period

II) Applies if you fall to pay your regular premium during the investment period |

I) Applies only for a certain period during the minimum investment period

II) Applies if you fail to pay your basic regular period during a certain period. |

| Partial withdrawal | The partial withdrawal charge is slightly higher up to the Policy’s account value. | The partial withdrawal is slightly lower up to the allowable amount. |

Single Premium Top-Ups

You can make a single premium top-up anytime during your policy term. The minimum amount allowed is S$1,000, which is used to invest in ILP sub-funds.

Premium Holiday

There is an “unlimited” premium holiday should you apply or stop making regular payments during the MIP.

However, premium holidays during the MIP will incur shortfall charges.

When in premium holiday, all applicable fees will be deducted from your units, thereafter reducing your account value.

You can continue making payments and the premium holiday will end.

Pass it On Option (Life Replacement Option)

You can pass the policy to your family or loved ones as a legacy gift.

Bonuses

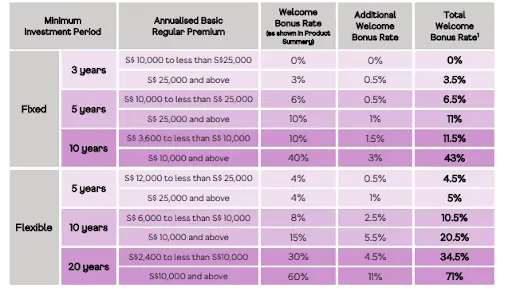

Welcome Bonus

You will get a welcome bonus after paying your basic regular premium for the first year of the policy. The sign-up bonus is calculated as follows;

Welcome Bonus = (The applicable rate) x (basic premium paid for the first year).

The welcome bonus is converted into extra units depending on your investment allocation.

However, you’ll not receive a welcome bonus under the following circumstances;

- For single top-ups,

- If you fail to pay your basic regular premiums in the first year of the policy.

The table below illustrates the welcome bonus rate for fixed and regular options under each investment period.

| 3-Years Fixed | 5-Years Fixed | 5-Years Flexible | 10-Years Fixed | 10-Years Flexible | 20-Years Flexible | |

| Yearly Regular Premium | S$10,000 to S$20,000 | S$10,000 to S$25,000 | Above S$12,000 | S$360 to S$10,000 | S$6,000 to S$10,000 | S$2,400 to S$10,000 |

| Welcome Bonus Rate | 0% | 6% | 4% | 10% | 8% | 30% |

| Yearly Regular Premium | Above 25,000 | Above S$25,000 | N/A | Above S$10,000 | Above S$10,000 | Above S$10,000 |

| Welcome Bonus Rate | 3% | 10% | N/A | 40% | 15% | 60% |

Loyalty Bonus

Under Singlife Savvy Invest, you also get to enjoy a Loyalty Bonus which is a percentage of your account value from the policy anniversary after the end of the minimum investment period.

The Loyalty Bonus is paid every year under the following conditions.

- Your policy is still running up to the point when your Loyalty Bonus is due

- You’ve not withdrawn from the policy in the past year up to when the bonus is due.

Here is a table illustrating the Loyalty Bonus payable to make things more straightforward.

| Loyalty Bonus | The Loyalty Bonus Rate |

| 1st – 10th Payment | 0.3% |

| 11th – 20th Payment | 0.4% |

| Above 21st Payment | 0.5% |

Even if you don’t qualify for a Loyalty Bonus during your policy anniversary, you can still qualify in subsequent years if you meet the stated conditions.

Promotions

The policy is currently running promotions for new customers (27 March 2022). However, it should be noted that these are promotions that can change at any time at the company’s discretion.

i) Additional Welcome Bonus

If you sign up now for the Singlife Savvy Invest, you can enjoy an additional welcome bonus of about 11%, as shown in the table below.

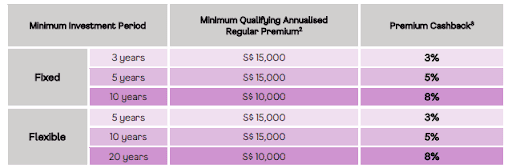

ii) Premium Cashback

When you sign up you can also earn a cashback of up to 8% as highlighted in the table below.

Protection

The plan has multiple benefits, such as the Terminal Illness and Death Benefit.

Further, to bump up your protection, you can add on the Supplementary Benefit, aka optional riders.

Life Stage Benefit

The Life Stage Benefit allows you to withdraw up to 10% of your account value as long as you meet the following conditions.

- The partial withdrawal amount is above S$500.

- The value of your account must be above S$1,000 after you partially withdraw.

- Submit your application within 90 days after the life stage event occurs.

- Show proof of the occurrence of the event.

Example of life stage events includes the following:

- Marriage,

- Divorce,

- Death of a spouse,

- Adoption,

- Birth,

- Purchase of property,

- If a child enrols for tertiary education,

- When you retire at 65 years,

- Upon hospitalisation.

The Life Stage Benefit is available up to 2 times during the policy’s term.

Additionally, you’ll not pay the partial withdrawal charge if you use the benefit during your minimum investment period. Also, the amount withdrawn will not reduce your allowed limit for partial withdrawal.

After the minimum investment period, you can still enjoy the Loyalty Bonus even if you’ve had a Life Stage Benefit.

Even so, the withdrawal shouldn’t exceed 10% of your account value at any time.

Death Benefit

The Death Benefit comes into force once the life assured passes on while the policy is still running. The amount paid is higher of;

- 101% of total basic regular premium + single premium top-up – partial withdrawals made OR;

- The account value.

The amount payable is minus any debts paid, and subsequently, the policy terminates.

Terminal Illness Benefit

The Terminal Illness benefit is available upon diagnosis of a terminal illness while the policy is still running.

You will be paid the benefit as an early payment for the Death Benefit as a single lump sum minus any debts to the policy.

Generally, Terminal Illness is a condition where death is expected within 12 months. However, this must be confirmed by a registered medical doctor.

A Terminal Illness due to HIV/AIDs related causes is excluded.

Optional Riders

The Singlife Savvy Invest has optional riders to bump up your protection.

Payer Premium Waiver Benefit

The Payer Premium Waiver Benefit offers protection against death, total and permanent disability(TPD), and Terminal Illness during the term of the policy.

With this benefit, all future premiums are waived in the event of death, TPD, or diagnosis of Terminal Illnesses.

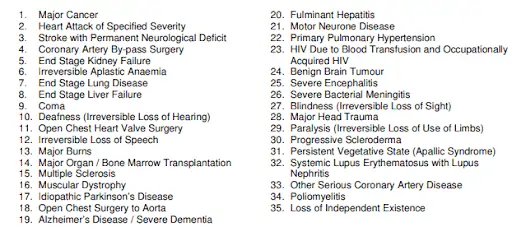

Payer Critical Illness Premium Waiver II

The Payer Critical Illness Premium Waiver II offers protection against critical illnesses during the policy term. The future premiums are waived in the event of a diagnosis with any of the following critical illnesses.

Fund Offerings

The Singlife Savvy Invest invests in unit trusts, and has about 100 funds directly invested instead of using an insurer sub-fund – which plays a large part in affecting your returns.

Also, the Savvy Invest gives access to certain accredited investor (AI) funds that are usually out of reach for retail investors.

This gives you the ability to generate much higher returns for yourself.

Other ILPs that offer this are the Tokio Marine #goTreasures, Tokio Marine GoClassic, and AXA Pulsar.

Singlife Savvy Invest Top Performing Funds

| Fund | 5-Year Annualised Returns |

| Fidelity Funds – Global Technology Fund | 22.5% |

| AB Sustainable US Thematic Portfolio USD | 20.7% |

| Global Technology Leaders Fund A2 USD | 18.1% |

| BGF World Mining Fund A2 USD | 15.6% |

| JPMorgan Funds – China Fund | 15.5% |

| BGF Sustainable Energy Fund Class A2 USD | 14.88% |

| Allianz Global Investors Fund A / AT | 14.79% |

| NIKKO AM SHENTON GLOBAL OPPORTUNITIES FUND | 13.37% |

| Infinity U.S. 500 Stock Index Fund | 13.0% |

| FSSA Regional China Fund | 12.5% |

Accurate as of 31 March 2022.

Before deciding on a fund, it’s essential to assess the company’s historical performance, if not sure, you can consult your financial advisor for guidance.

Singlife Savvy Invest Fees & Charges

The Singlife Savvy Invest has the following charges:

| Fee | Rates |

| Administrative fee | 0.65% p.a of the account value |

| Supplementary fee | 1.85% p.a of the account value for the first 10 years |

| Policy/Fund Switch Fee | – |

| Annual Management Fee | Depends on funds chosen |

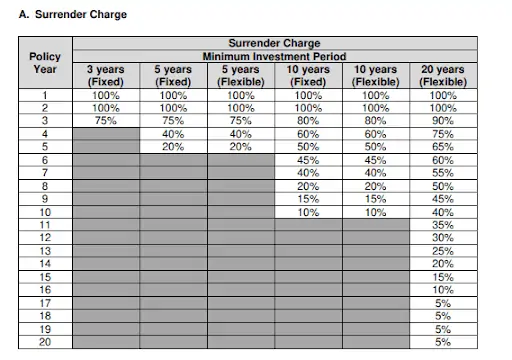

| Surrender Charge | The surrender value depends on the applicable rate, units surrendered and unit price of the ILP sub-fund.

|

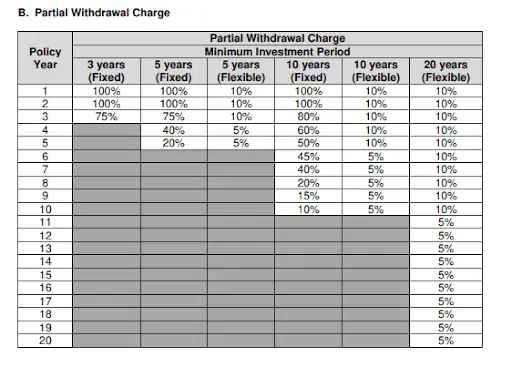

| Partial Withdrawal Charge | Minimum $500 if your account value does not fall below S$1,000.

A partial withdrawal charge is imposed if you make the withdrawal during the minimum investment period. Here is a schedule of the applicable charges.

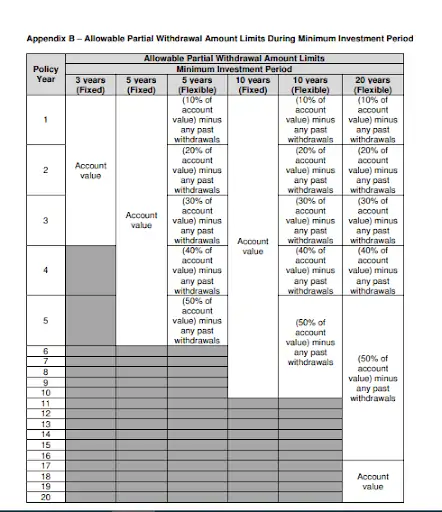

Here are the allowable limits during the minimum investment period

|

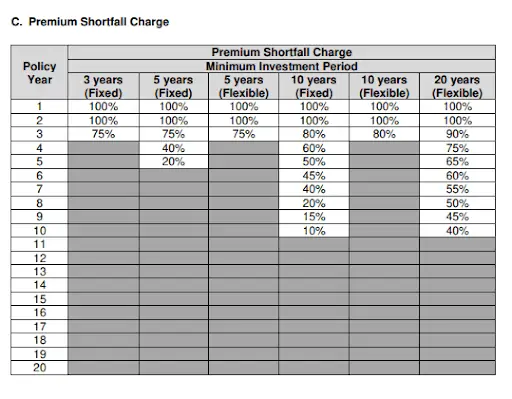

| Premium Shortfall Charge | If you fail to pay regular premiums during MIP.

|

| Single Premium Top-up | Free |

| Fund Switch | You get to enjoy unlimited fund switches at no cost during the policy term. The minimum amount allowed is S$1,000. |

Compulsory Fees

The Singlife Savvy Invest has a compulsory fee of 2.5% for the first 10 years, and 0.65% p.a thereafter.

Your compulsory fees are shown below:

- Administrative fee: 0.65% p.a. of account value

- Supplementary fee: 1.85% p.a. of account value for the first 10 years

Worth noting that the fees are one of the lowest in the market, similar to the Manulife InvestReady Wealth II!

How much will I receive upon maturity of the Singlife Savvy Invest?

We engaged a Singlife advisor, to do the calculation for you.

Assuming that you invest $200 monthly for 20 years and let it compound for another 10 years, the funds perform at 10% per annum, you made no withdrawals, and you did not take up any premium holidays; you can expect the below:

| First 10 Years | |

| Monthly premium: | $200 |

| Premium Payment Term: | 20 years (240 months) |

| Annual Fund Performance: | 10% |

| Fees in the first 10 years: | 2.5% |

| Net Fund Performance for the first 10 years: | 7.5% |

| Investment value: | $34,365.22 |

| Next 10 Years | |

| Fees in the next 10 years: | 0.65% |

| Net Fund Performance in the next 10 years: | 9.35% |

| Investment value: | $121,083.12 |

| Last 10 Years | |

| Fees in the last 10 years: | 0.65% |

| Net Fund Performance in the last 10 years: | 9.35% |

| Total Investment Value over 30 years: | $295,986.21 |

Total Premiums paid after 20 years: $48,000

Total Interest Earned: $247,986.21

ROI: 516.63%