With the ageing population and longer life expectancies of those living in Singapore, more and more elders need personal care and support services.

These services become necessary for individuals with disabilities.

The expenses related to severe disability can be challenging to handle without the support of insurance policies.

Eldershield, provided by the Singapore government, is an excellent solution to overcome these problems.

Although this covers anyone who has severe disabilities, Eldershield is explicitly designed for you when you’re old and require assistance.

The question is, is the income provided by this plan sufficient?

Should you get an Eldershield upgrade?

What is the best Eldershield upgrade plan?

Learn more about how this insurance plan works and how you can upgrade to a better plan.

What Is Eldershield?

Eldershield is a disability insurance coverage launched in September 2002 by the Singapore government for Singaporeans and those holding permanent resident status.

This insurance scheme covers those with severe disabilities.

In such a condition, the person cannot independently perform 3 or more daily essential activities, such as toileting, washing, feeding, mobility, transferring, and dressing.

The person insured with this plan receives a cash payout for up to 60-72 months every month.

This program is designed to provide some financial assistance to Singaporeans who need long-term care during their old age.

It supplements their savings when they have a severe disability. This plan has been replaced with CareShield Life from October 1, 2020.

Read more on Eldershield here.

Read more on CareShield Life here.

Find out the differences between Careshield vs Eldershied here.

Should You Upgrade Your Eldershield Policy?

It depends on several factors.

Do you think $400 every month for the next 6 years will be insufficient for your long-term care?

In that case, upgrading Eldershield might be a good decision.

You might also realise that after 6 years, having no income when you need it the most can be pretty scary.

Also, $400 worth of goods in 1999 cost $545 in 2019.

That’s a 36% in price change over 20 years in Singapore.

And if you assume a 2% inflation rate, in 20 years, $400 is worth $269.19.

Would $269.19 monthly for 6 years be enough to sustain you should you face severe disability?

If your answer is no, it’s probably best if you upgrade your Eldershield policy and get some supplements.

And if the cost of living isn’t enough to convince you to upgrade, studies have found that the amount of Singapore residents who will face any of the ADLs will be 2.5X by 2030 from 2010.

Imagine the numbers in 2040, 2050, and even 2060 – your probable golden years.

Even if you don’t have the extra cash to purchase these Eldershield supplements, the government has allowed you to pay using your Medisave for up to \$600 per year!

Benefits of Upgrading Early

There are several benefits if you upgrade your Eldershield policy early in life.

Firstly, the price you pay to get any Eldershield upgrades varies based on your entry age.

Any existing health conditions can also limit the coverage and require you to pay more.

For this reason, it is better to opt for it when you are young and healthy as it’s cheaper and will stay the same in the coming years.

This is especially true as you can opt for a higher payout for even lower premiums.

The payout amount differs from one company to another, but you can expect up to $5,000 a month, depending on the policy you get.

Professional care facilities will become accessible with a higher payout with more monthly income.

With the Eldershield supplement, you get protection for a lifetime and are not limited to 5-6 years of payment. You can continue receiving care services as long as you need them.

Some disabilities can only be managed and not treated, so a prolonged period payout is necessary – making the supplements a necessity – especially if you don’t have other sources of income when you’re severely disabled.

Most importantly, you will avoid becoming a burden on your family members with this financial assistance.

You can become eligible for Eldershield payout even if you fail to perform just 2 of the 6 activities of daily living.

By choosing this plan at an early age, your premiums will be cheaper and the benefits higher.

The Best Eldershield Upgrade

When upgrading your Eldershield, you can select from any plan offered by the 3 companies providing this coverage.

Supplements are offered by Singlife with Aviva, Great Eastern, and NTUC Income. They offer the Singlife ElderShield Standard & Plus, Eldershield Comprehensive and PrimeShield, respectively.

Irrespective of the company you selected for the coverage, you can upgrade to any plan they offer.

When selecting the right upgrade, pay attention to the plan that gives you the best value for money.

Look for the best return on premiums, lowest total premium, highest monthly allowance every month, and best coverage for every premium dollar.

Those at RetFree made this comparison below:

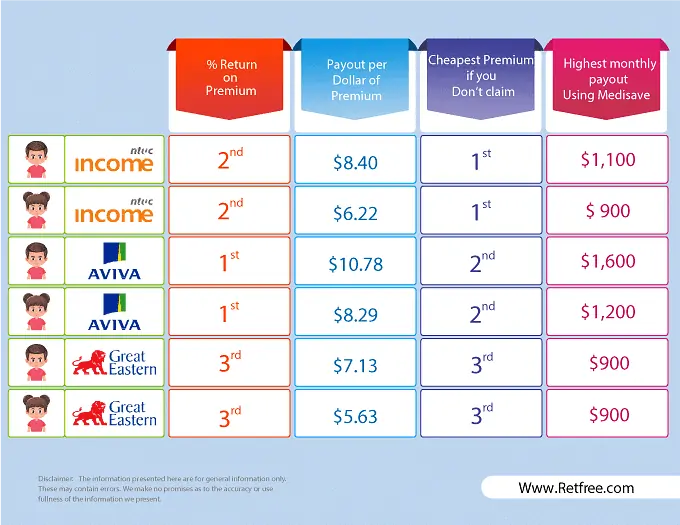

The Singlife ElderShield Standard (previously Aviva MyCare) provides the highest percentage of return on your premiums. Men can expect up to $10.78, and women can expect $8.29 in return for every $1 of premium.

NTUC Income offers the cheapest total premium if you make no claim. This amount will depend mostly on your age of entry and the choice of payouts you’re looking for.

For the Eldershield upgrade that offers the highest monthly payout, expect $1,600 for men and $1,200 every month for women under Singlife’s ElderShield Standard.

Next, we look at the features offered by each of the Eldershield supplement providers

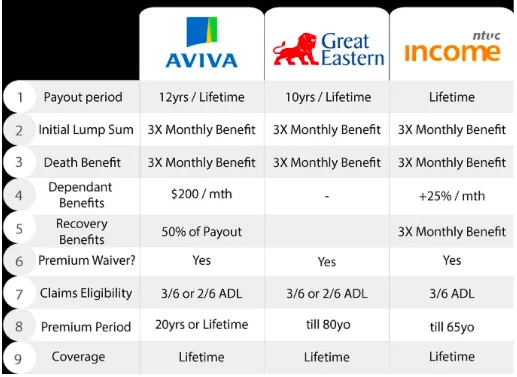

Dependent Benefits

Singlife with Aviva provides $200 every month of dependent benefits up to 36 months, while an extra 25% monthly benefit for 36 months under NTUC Income’s plan.

Recovery Benefits

If your physical condition improves, payouts for these Eldershield upgrades will stop.

However, Singlife ElderShield Standard allows you to claim half of the monthly payout still.

If you fully recover, NTUC Income provides a single payout that is 3 times the selected monthly benefit.

Do note that partial recovery is more likely to happen than full recovery, but it’s still an excellent benefit to have.

Number of ADLs Covered

Severe disability is usually defined as the inability to carry out 3 of the 6 activities of daily living.

However, Singlife ElderShield Standard and Great Eastern’s Eldershield Comprehensive provides the option to start receiving when you have only 2 of 6 ADLs.

Statistically, it’s less likely that you will face the inability to do 2 ADLs when compared to 3. If you look at the 6 ADLs, if you can’t do 2, chances are you can’t do 3 as well.

But there’s still a risk that you can’t do 2 ADLs, making you unable to receive payouts at all.

Therefore, this is something that you might want to consider.

Premium Payment Period

NTUC Income gives policyholders the option to stop paying premiums after reaching age 65.

Singlife with Aviva gives you the option to pay for 20 years or an entire lifetime.

On the other hand, Great Eastern offers only a single premium payment period that ends when you’re 80.

With a limited pay option, your premium amounts are generally higher due to shorter premium payment periods.

So if you’re looking for the cheapest premiums, chances are you should opt for more extended payment periods – but you should compare within each policy and not only across different insurers.

The best premium period is one that meets your specific needs. You can select premium for life because it will get you the lowest premium every year.

Our opinions on the best Eldershield upgrades are pretty much similar to RetFree’s recommendations.

Best Eldershield Upgrade for Highest Payouts – Singlife ElderShield Standard

![]()

The Singlife ElderShield Standard upgrade is your best bet if you are looking for the highest payout.

You can expect a $1,200 to $1,600 a month payout with your $600 yearly premiums paid from Medisave.

You can get higher payouts if you top up your premiums with cash.

The Singlife ElderShield Standard also provides the best value for your premiums.

Based on the total premiums you’ve paid, Singlife with Aviva will pay you more for each dollar of premium.

Cheapest Eldershield Upgrade – NTUC Income PrimeShield

![]()

Opt for NTUC Income’s PrimeShield if you are looking for the lowest premium option. Note that the low premium is only if a claim is not made.

So if you make any claims, be prepared to pay more.

Best Eldershield Upgrade for 2 of 6 ADLs – Singlife ElderShield Standard/Plus

Use Singlife with Aviva or Great Eastern’s Eldershield supplements if you want the claim definition to be limited to 2 ADLs.

From here, you can compare which one has the highest payout and lowest premiums for 2 ADL claims.

Based on the comparisons mentioned above, the Singlife ElderShield Standard has better premium to payout value, and it’s what you should consider if 2/6 ADL is what you’re looking for.