How do you choose the right asset allocation for your portfolio? This is a question that many investors struggle with.

There are so many different options available, and it can be difficult to know which one is right for you.

In this blog post, we will discuss the different types of portfolio allocation models and provide some tips on how to choose the right one for your needs.

We will also talk about asset allocation strategies and explain why they are important.

By the end of this post, you will have a better understanding of asset allocation and how it can help you reach your investment goals!

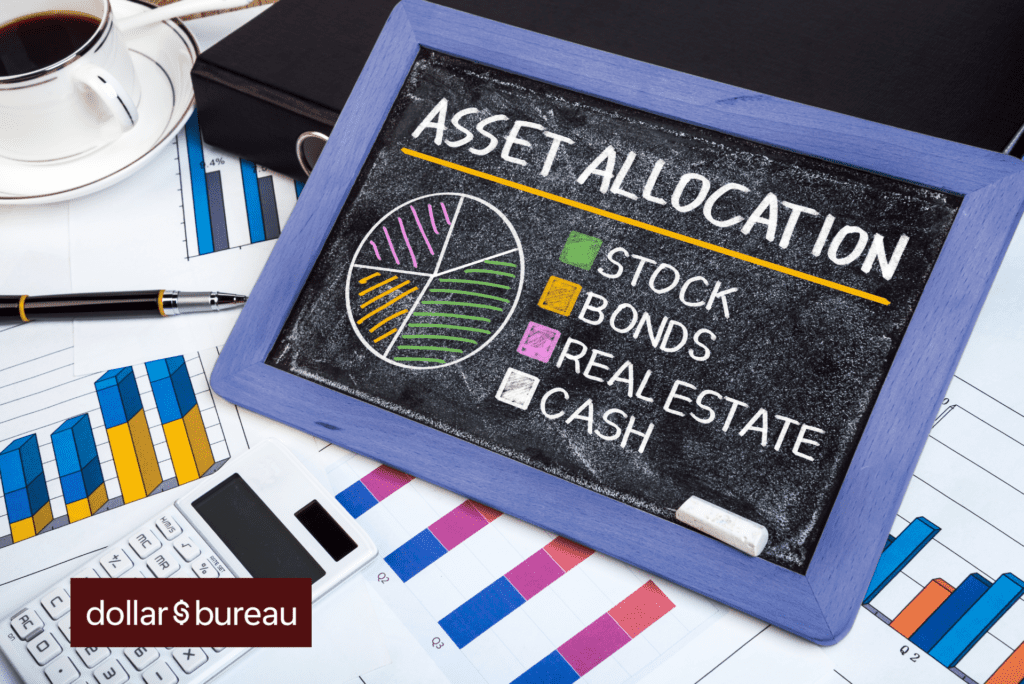

What Is Asset Allocation?

Asset allocation is the process of dividing your investment portfolio among different asset classes, such as stocks, bonds, and cash.

For example, you might allocate 60% of your portfolio to stocks, 30% to bonds, and the remaining 10% to alternative assets.

The options are endless and it comes down to what you are comfortable with.

An asset is anything that has value and can be sold for a price. Allocation is how you weigh your assets in your portfolio.

Another way to think of asset allocation is to imagine a pie.

Each asset class would be a slice of that pie. You can have a large or small slice of each asset, but the key is to have a diversified pie.

That way, if one asset class underperforms, the others can help offset those losses.

If your asset allocation is optimised, you should be able to watch your investments grow over time!

Why Is Asset Allocation Important?

Asset allocation is important because it can help you reach your investment goals while keeping within your risk tolerance.

Diversifying your investments will help to protect you from market volatility and reduce the overall risk of your portfolio.

Another reason why asset allocation is important is that it can help you improve your risk/reward ratio.

This means that you will be able to make more money while taking on less risk.

As an investor, this is important because it allows you to reach your financial goals while minimising the chance of losing money.

There are many different types of asset allocation models, each with its own unique benefits and risks.

The most common types of asset allocation models are:

- Conservative

- Moderately Conservative

- Moderately Aggressive

- Aggressive

- Very Aggressive

Make sure to keep reading because we will go over each in more detail to help you decide which one is right for you!

What Is The Goal of Asset Allocation?

The goal of asset allocation is to diversify your investments and minimise risk while still achieving your desired return.

Simply put, it is the process of deciding how to allocate your assets to reach your financial goals.

Here are the 2 main goals that should be strived for when selecting an asset allocation.

- Maximising returns while lowering risks

- Keep within your risk tolerance

If you can achieve both of these goals, then you are well on your way to selecting the right asset allocation for your portfolio.

Here is a more detailed look at each goal.

Maximising Returns While Lowering Risks

This goal is all about making as much money as possible while taking on the least amount of risk.

It is important to remember that there is always a trade-off between risk and reward.

To make more money, you usually will need to take on more risks.

However, if you are not comfortable with taking on a lot of risks, you can still make money by investing in lower-risk assets.

The key is to find the right balance for you. Asset allocation can help you do this by allowing you to diversify your investments and choose how much risk you are willing to take on.

As an investor, it’s best to allocate capital towards ‘asymmetric bets’.

By finding assets that have a higher increase potential than decrease potential, you can make more money while taking on less risk.

With these types of investments, you can potentially make a lot of money even with a small allocation.

So when you’re looking at investments, not only are high returns important but how much risk you’re taking to get those returns should be considered too.

50% return in a year sounds amazing, but if you’re risking 80% of your money for only 50% returns, it might not sound that logical.

Unless of course, you are risk tolerant.

Keep Within Your Risk Tolerance

This goal is all about ensuring that you do not take on more risks than you are comfortable with.

Investing in the stock market can be very risky. If you are not comfortable with taking on a lot of risks, it is important to allocate your assets accordingly.

For example, if you are risk-averse, you might want to allocate a larger portion of your portfolio to cash and bonds.

On the other hand, if you are willing to take on more risks, you might want to allocate a larger portion of your portfolio to stocks.

As long as the allocation does not emotionally drain you when the market drops or has the potential financially destroy you, it is considered to be within your risk tolerance.

Now that we have gone over the goals of asset allocation, let’s take a more detailed look at the different types of asset allocation models.

Types of Portfolio Allocation Models

These models are just that, models. There is no perfect portfolio, and the best portfolio is the one that is right for you.

Every investor has different goals, needs, and risk tolerances. As a result, there is no one-size-fits-all asset allocation model.

However, these models can serve as a helpful starting point for you to create your own portfolio.

Asset Allocation Model #1 – Conservative

A conservative asset allocation typically has a lower percentage of stocks and a higher percentage of bonds.

The goal of this allocation is to provide stability and preserve capital. This model is best suited for investors who are risk-averse and are looking for stability and income.

It is unlikely that you will find assets such as penny stocks, cryptocurrencies, or high-yield bonds in a conservative portfolio.

Instead, you are more likely to find assets such as blue-chip stocks and investment-grade bonds.

Real-estate investment trusts (REITs) are also a common asset in conservative portfolios. REITs tend to be less volatile than stocks and can provide a steady stream of income.

Exchanged Traded Funds (ETFs) are also a popular choice for conservative investors. ETFs are a type of investment that tracks an index, sector, or asset class.

They are generally lower risk than individual stocks and can be a good way to diversify your portfolio.

When it comes to commodities, conservative investors typically avoid them.

This is because commodities are more volatile than other asset classes and can be a significant source of risk.

Alternative asset classes such as art, wine, and collectibles are also typically avoided by conservative investors. This is because these assets are often illiquid and can be difficult to value.

The weighting of each asset class will vary depending on the individual’s goals and risk tolerance. However, a typical conservative portfolio might look something like this:

- 20% REITs (Real Estate Investment Trusts)

- 20% Equities (Blue Chip Companies)

- 20% Bonds (Investment Grade)

- 40% ETFs (S&P 500)

As you can see, ETFs make up the majority of a conservative portfolio. This is because they are lower risk and can help to diversify your investments.

Rather than picking individual stocks or trusting in the government to pay back its debt, you are investing in a basket of assets.

REITs are also a popular choice for conservative investors as they can provide stability and income.

They are less correlated with the stock market than stocks and can help to diversify your portfolio.

Asset Allocation Model #2 – Moderately Conservative

A moderately conservative asset allocation typically has a slightly higher percentage of stocks and a slightly lower percentage of bonds than a conservative portfolio.

The goal of this allocation is to provide stability and potential capital appreciation.

This model is best suited for investors who are looking for stability and income but are willing to take on a little bit more risk.

As with a conservative portfolio, you are unlikely to find riskier assets such as stocks that have the potential to generate high returns.

However, you may find a slightly higher percentage of stocks in a moderately conservative portfolio than you would in a conservative portfolio.

This is because stocks have the potential to provide capital appreciation.

REITs are also a common asset in moderately conservative portfolios. This is because real estate is known for being a relatively stable asset class.

REITs also have the potential to provide income and capital appreciation.

There might be a small percentage of commodities and alternative asset classes in a moderately conservative portfolio.

This is because these assets can provide diversification and potential capital appreciation. Here is what a typical moderately conservative portfolio might look like:

- 20% REITs (Real Estate Investment Trusts)

- 40% Equities (Blue Chip Companies)

- 15% Bonds (Investment Grade)

- 20% ETFs (S&P 500)

- 2.5% (Gold)

- 2.5% (Art)

The reason why equities make up a larger percentage of a moderately conservative portfolio is that they have the potential to provide capital appreciation.

This is the main goal of this asset allocation. However, they are still blue-chip companies that are relatively stable.

These companies usually pay out dividends which can provide income.

The combined 55% allocation of REITs, ETFs, and bonds should help to stabilise the portfolio in times of market uncertainty.

Commodities and alternative assets are also included to provide diversification and potential capital appreciation.

The reason why gold is the commodity of choice is that it is known for being a safe haven asset. This means that it tends to hold its value or increase in value when other assets are losing value.

Art is included as an alternative asset because it can be a good store of value and has the potential to appreciate in value over time. It is usually not correlated with other asset classes which makes it a good diversifier.

Asset Allocation Model #3 – Moderately Aggressive

A moderately aggressive portfolio has a higher percentage of stocks than a conservative or moderately conservative portfolio.

The goal of this asset allocation is to provide capital appreciation.

This model is best suited for investors who are looking for growth but are willing to take on a moderate amount of risk.

Cryptocurrencies, small-cap stocks, and emerging markets stocks are examples of assets that you might find in a moderately aggressive portfolio.

REITs are also a common asset in this type of portfolio. This is because they can provide income and stability.

However, the percentage of REITs will be lower than in a conservative or moderately conservative portfolio because the focus is on growth.

ETFs can still play a role but they might be more industry-focused. For example, ARK Innovation ETF (ARKK) is a technology-focused ETF.

This would be a good choice for an investor who wants exposure to tech stocks but doesn’t want to pick individual stocks.

The percentage of bonds will be lower than in a conservative or moderately conservative portfolio because the goal is capital appreciation.

However, bonds can still provide stability and income. Here is what a typical moderately aggressive portfolio might look like:

- 50% Equities (Tech Stocks/Growth Companies)

- 10% Cryptocurrencies (BTC & ETH)

- 20% ETFs (Sector Specific)

- 10% REITs

- 5% Bonds

- 2.5% Commodities

- 2.5% Alternative Investments

When it comes to moderately aggressive portfolios, the key is to remember that aggression should not mean reckless.

The 10% cryptocurrencies position is an asymmetric bet and is focused on the two largest and most liquid cryptocurrencies, Bitcoin and Ethereum.

The 20% ETFs position is also focused on sector-specific funds which will provide exposure to different industries. This will help to diversify the portfolio and reduce risk.

However, specific tracking allows taking advantage of growing industries.

50% equities in tech and growth are where the aggressiveness comes in. This focuses on companies that have the potential to provide capital appreciation.

These are usually more volatile than blue-chip stocks but they also have the potential to provide higher returns.

REITs, commodities, and bonds make up the last 17.5% of the portfolio. This is where stability and diversification come in.

Some of the commodities may be in gold but other options such as silver, oil, and gas are also available.

These asset classes are less volatile and provide a hedge against market uncertainty.

When it comes to alternative investments, collectibles and strong NFT projects might make their way into this portfolio.

These alternative investments are of higher risks and thus have low allocations, however, they give you exposure and the ability to generate more risk-adjusted returns.

The goal of a moderately aggressive portfolio is to provide capital appreciation while still diversifying the portfolio and reducing risk.

This portfolio is best suited for investors who have a longer time horizon and a stronger risk tolerance.

Asset Allocation Model #4 – Aggressive

This is where you put most of your money into stocks to earn a higher return.

An aggressive portfolio has more risk but also has the potential to generate greater returns over time than a conservative portfolio.

The aggressive portfolio is best suited for investors who are willing to take on more risk to achieve their financial goals.

This type of investor is typically younger and has a longer investment horizon. They may also have a higher tolerance for volatility and are comfortable with the idea of losing money in the short term in exchange for the chance to earn higher returns over the long term.

If you’re an aggressive investor, you should consider investing in a mix of domestic and international stocks, as well as growth and value stocks.

You may also want to add some exposure to real estate and commodities. Here is an example of what an aggressive portfolio might look like:

- 60% Equities (Domestic & International / Value & Growth Companies)

- 15% Cryptocurrencies (5% BTC / 5% ETH / 5% Altcoins)

- 10% Real Estate

- 5% Commodities

- 5% ETFs (Emerging Markets)

- 2.5% Alternative Investments

- 2.5% Equity Crowdfunding

From this allocation example, you can see that the bulk of an aggressive investor’s portfolio is in stocks.

This is because stocks have the potential to generate the highest returns over time.

The downside protection comes from the other asset classes (real estate and safe commodities) that are included in the portfolio.

Cryptocurrencies are an aggressive addition at 15% and 5% being altcoins. This means that the investor is comfortable with the volatility and potential for loss to achieve higher returns.

Emerging markets are also a more volatile asset class but have the potential for higher returns. This is why they make up a small portion of the portfolio at just ETFs.

Equity crowdfunding is introduced into this portfolio as a new asset class. This, along with alternative investments can provide high returns but is also very risky.

However, by including these asset classes in a small portion of the portfolio, it can help to boost returns while still diversifying the portfolio.

The aggressive portfolio is not for everyone. If you’re risk-averse or have a shorter investment horizon, this may not be the right asset allocation for you.

Asset Allocation Model #5 – Very Aggressive

This portfolio is for investors who are willing to take on a high level of risk to achieve their financial goals.

This means that the portfolio will be made up of mostly stocks, cryptocurrencies, and other creative investment options.

The goal is to achieve high returns, but there is also a higher chance of losses. Here is an example of what a very aggressive portfolio might look like:

- 60% Equities (50% Growth / 20% Penny Stocks / 30% Small Cap)

- 25% Cryptocurrencies (10% BTC / 7.5% ETH / 7.5% Altcoins)

- 10% Equity Crowdfunding

- 5% Alternative Investments

The very aggressive portfolio is best suited for investors with a long-term time horizon and a high tolerance for risk.

If you are retired or close to retirement, this portfolio is not recommended as it could jeopardise your financial security.

The 5% alternative investing can be anything from Bitcoin mining to investing in a friend’s business or even sports cards and NFTs.

This requires a higher level of understanding of each individual asset, but the returns can be high if done correctly.

A 10% equity crowdfunding position allows the aggressive investor to get into early-stage pre-IPO companies.

This is a higher risk/reward investment but can provide great returns if the company is successful.

The 25% position of cryptocurrencies is allocated to Bitcoin, Ethereum, and altcoins.

The aggressive investor has conviction in the global adoption and potential of cryptocurrencies.

There are no commodities because Bitcoin is believed to be a stronger store of value, although this is an aggressive stance.

The positioning of 60% in equities is allocated to growth stocks, penny stocks, and small-cap stocks.

This is a very broad and risky allocation, but these types of equities typically have more room to grow. If they are participating in an innovative or growing industry, the returns could be high.

This portfolio is not for everyone, but if you have a high-risk tolerance and are willing to stomach some losses, it could be a good fit for you.

Alternatively, if you’re not one looking to explore other asset classes apart from stocks, REITs, and bonds, many investors adopting the very aggressive asset allocation model have 100% in equities.

These stocks are then allocated according to growth, value, and blue-chip stocks in order to better balance their risks.

Asset Allocation Strategies

Now that we have gone over the different types of asset allocation models, it’s time to choose the right one for you.

By understanding these 3 main strategies, you can select the most appropriate allocation model or adjust them to fit your needs.

Remember that no model is perfect, and you should always review your portfolio periodically to make sure it still aligns with your goals and strategy.

Strategic Asset Allocation

This entails a predetermined asset allocation for each category and portfolio readjustment regularly.

The strategic asset allocation requires rebalancing to meet the allowed weighting.

For example, if the portfolio’s goals are to have 10% into cryptocurrencies and they grow to become 20% of the portfolio, then selling some of the cryptocurrency holdings to get back to the original target.

Tactical Asset Allocation

TAA is an active management strategy that aims to take advantage of short-term market movements.

This type of asset allocation can be used to overweight or underweight specific asset classes based on market conditions.

For example, if the market is bearish and you expect a recession, you might want to underweight stocks and increase your allocation to bonds.

Adjusting allocation sizes based on market conditions allow for a more fluid and adaptable investment style.

However, it requires a greater knowledge of economic cycles and overall market conditions.

This strategy might not be the best for the passive investor.

Dynamic Asset Allocation

DAA is a variation of TAA that also considers the best and worst-performing assets.

By selling off the underperforming and adding to the top-performing assets, this strategy can help improve returns and manage risk.

For example, if a stock has not lost 5% of value in the past 2-3 years but Bitcoin has gone up 100%, a DAA strategy would be to sell some of the stock and buy Bitcoin.

If the bull thesis for Bitcoin still is in play and the company’s stock will not perform well in the next few years, then this would be an ideal time to allocate more to the higher potential growth asset.

DAA is a more active management style and requires ongoing monitoring. This strategy is not for the investor who wants to set it and forget it.

How To Decide Which Allocation & Strategy Is Right For You

There are many different ways to go about asset allocation, and the right strategy for you will depend on your individual circumstances.

However, some general tips can help you choose the right asset allocation for your needs.

Some things to consider include:

- Your investment goals

- Your risk tolerance

- Your time horizon

- Your need for liquidity

Investment Goals

By understanding your goals and objectives, you can develop a clear investment strategy.

From there, you can start to build out your portfolio with the right asset allocation. Your investment goals should be specific, measurable, achievable, relevant, and time-bound.

A specific goal would be something like, “I want to have $___ amount in my investment portfolio by the time I’m ____.”

To measure your progress, you can track the value of your portfolio regularly. Having an investment journal can also help you track your progress and reflect on your successes and failures.

Achievable goals are also important because if they are unrealistic, you might feel discouraged when you don’t reach them. Make sure your goals are challenging but achievable.

Relevancy also matters because you don’t want to set goals that are no longer relevant to your situation. For example, if you’re retired, you might not be as concerned with growth potential and more focused on preserving your capital.

Finally, time-bound goals help you stay on track and motivated. If your goal is to retire in 15 years, you’ll want to make sure your asset allocation is appropriate for that timeline.

Oh, and yes, you must also know how active you want to be in your investment journey.

Do you find it fun to constantly read the news and adjust your portfolios based on opportunities?

Or would you rather take a more passive approach and only check on them every quarter, 6 months, or a year?

Depending on your answers for this, it’ll determine which allocation model and strategy you should take.

Risk Tolerance

This is one of the most important factors to consider when allocating assets. Risk tolerance is the amount of risk you’re willing to take on in pursuit of your investment goals.

There are many different ways to measure risk tolerance. Some people use a questionnaire, while others base it on their personal circumstances.

Some simply base it on how well they sleep at night during turbulent market conditions.

If you are anxious and constantly checking your portfolio’s value during down markets, you have an allocation that requires a higher risk tolerance than what you’re comfortable with.

Generally, your risk tolerance will fall into one of 3 categories: conservative, moderate, or aggressive.

Understanding your risk tolerance will help you better understand which asset allocation model would be best for you.

Your Time Horizon

Each investment should have a time horizon. Some positions in your portfolio might only have a short-term time horizon, while others might be part of your long-term strategy.

For example, if you’re invested in equity crowdfunding, you might sell right away if the company goes public or is acquired.

But if you’re investing in real estate or Bitcoin, you might not ever sell and decide to pass it on to your heirs.

Your time horizon will also help determine your risk tolerance. The longer your time horizon, the more risk you can take on because you have time to recover from any losses.

If you’re retired and need to generate income, you might have a shorter time horizon and be more conservative with your asset allocation.

Need for Liquidity

This is another important factor to consider, especially if you have a shorter time horizon.

By understanding illiquid and liquid assets, you can adjust your allocation as needed.

Some positions might have to be a part of your portfolio for many years and knowing this beforehand is essential as an investor.

Liquidity refers to how quickly you can access your money. For example, cash is the most liquid asset because you can access it immediately.

Other assets, such as real estate or art, can take longer to sell and are less liquid.

If you need to access your money quickly, you’ll want to have a higher allocation to cash and other liquid assets.

Conversely, if you’re investing for the long term, you might be less concerned with liquidity and more focused on growth potential.

Conclusion

Choosing the right asset allocation can be a daunting task, but it is a crucial part of ensuring your financial security.

There is no perfect allocation that will work for everyone, but there are some general guidelines that can help you choose the right mix of investments for your needs.

Consider your investment goals and risk tolerance when choosing your asset allocation.

A diversified portfolio with a mix of stocks, bonds, and cash can help you reach your goals while minimising risk.

Review your asset allocation periodically to make sure it still meets your needs and rebalance as necessary.

The most important thing to remember is that there is no one-size-fits-all solution. The right asset allocation for you will depend on your individual circumstances.

But by following these tips, you can create a portfolio that matches the strategy that works best for you.

Thanks for taking the time to better understand asset allocations when it comes to investing!

Should you rather outsource investing, we partner with MAS-licensed financial advisors to help you with this.