Travelling somewhere can be exciting, depending on the reasons for your travelling, whether personal, business or holiday travel.

But sometimes events that are not planned can take place while you are travelling.

Singlife Travel Insurance is comprehensive and provides solutions for many scenarios of what can happen while travelling.

Keep reading for our review of the Singlife Travel Insurance.

Key Features Of Singlife Travel Insurance

Singlife offers some tremendous key features, and when considering your options, it is always important to stay informed and know what you are buying.

Below are some highlights of Singlife Travel Insurance.

Diverse Medical Coverage: Singlife Travel Insurance offers a range of medical coverage, with its Prestige tier providing unlimited overseas medical expenses.

Competitive COVID-19 Provisions: Across its tiers, Singlife offers substantial COVID-19-related benefits, including overseas medical expenses and emergency medical evacuation due to the virus.

Personal Accident Benefits: Singlife provides significant personal accident benefits, ensuring travellers are covered in case of unforeseen incidents.

Baggage and Personal Belongings Protection: Singlife offers competitive coverage for lost or damaged baggage and personal belongings, safeguarding travellers’ possessions.

Value for Money: With its range of benefits and competitive premiums, Singlife Travel Insurance offers a balanced cost-to-benefit ratio, making it a valuable choice for various travellers.

Adventure Sports Inclusion: Specifically covers adventurous water sports, extending various protections like accidental death, permanent disablement, and equipment loss or damage.

Equipment Hire Coverage: Compensates for the hiring cost of replacement water sports equipment in case of accidental loss, damage, or significant delays.

These features represent a blend of standard and unique aspects of Singlife Travel Insurance, emphasising its coverage of typical travel incidents and specific adventurous activities.

Comparison Against Other Single-Trip Travel Insurance Policies

In this section, the insurers that we’re comparing Singlife Travel Insurance against its competitors:

- AIG Travel Guard Direct

- AIA Around the World Plus (II)

- Allianz Travel Bronze

- Klook TravelCare

- MSIG TravelEasy

- NTUC Income Travel Insurance

- Sompo Travel (COVID-19) Insurance

- Etiqa TIQ Travel Insurance (with COVID-19 cover)

- FWD Travel Insurance Plan.

The basis for this comparison will be the coverage for an individual travelling to ASEAN for a week and the lowest-tiered plan across all insurers.

Travel Insurance Plan | Total Premium | Overseas Medical Expenses | Accidental Death & TPD | Overseas Travel Delay ($100 for every 6 hours) | Trip Cancellation on (death, illness, and natural disaster) | Baggage Delay ($200 every 6 hours) | Baggage Loss/Damage | Cost-to-Benefit Ratio |

AIG Travel Guard Direct Basic | S$83.00 | S$50,000 | NA | S$200 | S$2,500 | NA | S$3,000 | 671.08 |

Singlife Travel Insurance Lite | S$49.36 | S$250,000 | S$50,000 | S$500 | S$5,000 | S$500 | S$3,000 | 6260.13 |

AIA Around the World Plus (II) Classic | S$55.45 | S$200,000 | S$150,000 | S$1,000 | S$5,000 | S$1,000 | S$3,000 | 6492.34 |

Allianz Travel Bronze | S$36.96 | S$200,000 | S$50,000 | S$500 | S$5,000 | S$500 | NA | 6926.40 |

Sompo Travel (COVID-19) Insurance Essential | S$48.00 | S$200,000 | S$200,000 | S$800 | S$5,000 | S$1,200 | S$1,000 | 8500 |

FWD Travel Insurance Premium + COVID-19 Enhanced Travel Benefits | S$32.40 +S $12.44 = S$44.84 | S$200,000 | S$200,000 | S$300 | S$7,500 | S$150 | S$3,000 | 9168.15 |

NTUC Income Travel Insurance Classic | S$36.60 | S$250,000 | S$100,000 | S$1,000 | S$5,000 | S$1,000 | S$3,000 | 9836.07 |

MSIG TravelEasy Standard | S$37.20 | S$250,000 | S$150,000 | S$500 | S$5,000 | S$600 | S$3,000 | 10997.31 |

Etiqa TIQ Travel Insurance Entry (with COVID-19 cover) | S$34.20 | S$200,000 | S$200,000 | S$300 | S$5,000 | S$200 | S$2,000 | 11915.20 |

Klook TravelCare Lite | S$27.65 | S$150,000 | S$200,000 | S$400 | S$5,000 | S$400 | S$3,000 | 12976.49 |

There will also be an add-on for COVID-19 benefits.

In comparing Singlife Travel Insurance with other insurance policies in Singapore, focusing on single-trip policies for ASEAN travel, we observe the following:

- Premium Affordability: Singlife Travel Insurance Lite, priced at $49.36, is competitively priced. It’s more affordable than AIG Travel Guard Direct Basic and AIA Around the World Plus (II) Classic, but slightly higher than Allianz Travel Bronze and Etiqa TIQ Travel Insurance Entry.

- Overseas Medical Expenses Coverage: Singlife offers a high coverage amount of $250,000, which is on par with NTUC Income Travel Insurance Classic and MSIG TravelEasy Standard, and higher than AIG, AIA, Allianz, Sompo, FWD, and Etiqa.

- Accidental Death and TPD: Singlife’s coverage of $50,000 is moderate compared to others. It’s equal to Allianz Travel Bronze but lower than AIA, Sompo, FWD, NTUC Income, MSIG, and Etiqa, which offer higher coverage in this category.

- Overseas Travel Delay Compensation: Singlife’s $500 compensation is competitive, matching Allianz and MSIG, and surpassing AIG and Etiqa. However, it’s less than AIA, Sompo, FWD, and NTUC Income.

- Trip Cancellation Coverage: Singlife provides a $5,000 coverage, which is consistent with most other insurers except AIG, which offers a lower amount.

- Baggage Delay Compensation: Singlife’s $500 is higher than FWD and Etiqa but lower than Sompo and NTUC Income. AIG and Allianz do not offer this benefit.

- Baggage Loss/Damage: Singlife’s coverage of $3,000 is standard among most plans, except for Sompo and Etiqa, which offer lower amounts. Allianz Travel Bronze does not provide this coverage.

- Cost-to-Benefit Ratio: Singlife stands out with a high cost-to-benefit ratio of 6260.13, indicating a favorable balance between cost and coverage, especially in comparison to AIG, AIA, Allianz, and Etiqa.

Comparison Against Other Annual-Trip Travel Insurance Policies

Next up, let’s compare the insurers for annual trips. (We’ve removed Sompo Travel Insurance here because they do not offer travel insurance for annual trips.)

The basis for this comparison will be the coverage for a single individual travelling to ASEAN for an annual trip and the lowest-tiered plan across all insurers.

Travel Insurance Plan | Total Premium | Overseas Medical Expenses | Accidental Death & TPD | Overseas Travel Delay (S$100 for every 6 hours) | Trip Cancellation(death, illness, and natural disaster) | Baggage Delay (S$200 every 6 hours) | Baggage Loss/Damage | Cost-to-Benefit Ratio |

AIG Travel Guard Direct Basic | S$554.00 | S$50,000 | NA | S$200 | S$2,500 | NA | S$3000 | 100.54 |

Allianz Travel Bronze | S$570.60 | S$200,000 | S$50,000 | S$500 | S$5,000 | S$500 | NA | 448.65 |

NTUC Income Travel Insurance Classic | S$495.90 | S$250,000 | S$100,000 | S$1,000 | S$5,000 | S$1,000 | S$3,000 | 725.95 |

Singlife Travel Insurance Lite | S$460.00 | S$250,000 | S$50,000 | S$500 | S$5,000 | S$500 | S$3,000 | 769.57 |

AIA Around the World Plus (II) Classic | S$460.50 | S$200,000 | S$150,000 | S$1,000 | S$5,000 | S$1,000 | S$3,000 | 781.76 |

MSIG TravelEasy Standard | S$447.20 | S$250,000 | S$150,000 | S$500 | S$5,000 | S$600 | S$3,000 | 914.80 |

Etiqa TIQ Travel Insurance Entry (with COVID-19 cover) | S$369.00 | S$200,000 | S$200,000 | S$300 | S$5,000 | S$200 | S$2,000 | 1104.34 |

FWD Travel Insurance Premium + COVID-19 Enhanced Travel Benefits | S$259.55 + S$37.54 = S$351.88 | S$200,000 | S$200,000 | S$300 | S$7,500 | S$150 | S$3,000 | 1168.29 |

Here’s a comparison of Singlife Travel Insurance against other annual trip policies:

- Total Premium: Singlife Travel Insurance Lite is priced at $460.00, making it a mid-range option. It’s more affordable than AIG Travel Guard Direct Basic, Allianz Travel Bronze, and NTUC Income Travel Insurance Classic, but slightly more expensive than FWD Travel Insurance Premium and Etiqa TIQ Travel Insurance Entry.

- Overseas Medical Expenses: Singlife offers a high coverage amount of $250,000, matching MSIG TravelEasy Standard and NTUC Income Travel Insurance Classic, and surpassing AIG, AIA, Allianz, FWD, and Etiqa.

- Accidental Death & TPD: Singlife’s coverage of $50,000 is lower compared to most other plans, except Allianz Travel Bronze. AIA, FWD, MSIG, NTUC Income, and Etiqa offer higher coverage in this category.

- Overseas Travel Delay Compensation: Singlife provides $500, which is on par with Allianz and MSIG, and higher than FWD and Etiqa. However, it’s less than AIA and NTUC Income.

- Trip Cancellation Coverage: Singlife, along with AIA, Allianz, MSIG, and NTUC Income, offers a $5,000 coverage, which is higher than AIG and lower than FWD.

- Baggage Delay Compensation: Singlife’s $500 is competitive, matching Allianz and MSIG, and surpassing FWD and Etiqa. NTUC Income offers a higher compensation.

- Baggage Loss/Damage: Singlife’s coverage of $3,000 is standard among most plans, except for Etiqa, which offers a lower amount. Allianz Travel Bronze does not provide this coverage.

- Cost-to-Benefit Ratio: Singlife’s ratio of 769.57 indicates a good balance between cost and coverage, especially when compared to AIG and Allianz. However, it’s lower than FWD, MSIG, NTUC Income, and Etiqa.

Who Is Singlife Travel Insurance Prestige Best Suited For:

Frequent International Business Travellers

Given the comprehensive features of Singlife Travel Insurance Prestige, it is particularly well-suited for frequent international business travellers.

Here’s why:

Comprehensive Medical Coverage: Business travellers often have tight schedules and cannot afford prolonged medical disruptions.

The unlimited overseas medical expense coverage offered by Singlife ensures they receive the best medical care without worrying about costs, especially in countries with high medical expenses.

COVID-19 Considerations: Business travellers must be especially cautious about COVID-19 in the current global context.

Singlife’s substantial coverage related to the virus, including overseas medical expenses and emergency medical evacuation, provides an added layer of security.

Personal Accident Benefit: Business trips involve various modes of transportation and activities, increasing the risk of accidents.

Singlife’s significant personal accident benefit ensures that travellers are well-covered in case of unforeseen incidents.

Efficiency in Trip Disruptions: Business travellers can’t afford significant delays or cancellations.

While Singlife offers competitive coverage in these areas, its standout medical benefits ensure that health-related disruptions are addressed efficiently.

Adventure Enthusiasts And Solo Backpackers

Singlife Travel Insurance Prestige is an excellent fit for adventure enthusiasts and solo backpackers. Here’s the rationale:

Unparalleled Medical Coverage: Adventure enthusiasts often venture into remote areas or engage in activities that carry inherent risks.

The unlimited overseas medical expenses coverage by Singlife ensures that should they encounter any health issues, they can access the best medical care without being burdened by costs.

Personal Accident Benefit: Solo backpackers and adventure seekers are more exposed to unforeseen incidents, given the nature of their travels.

The substantial personal accident benefit of S$500,000 Singlife provides a safety net, ensuring they’re covered in unexpected accidents.

COVID-19 Coverage: In these times, even the most intrepid travellers need to be cautious about the pandemic.

Singlife’s comprehensive COVID-19 coverage, including medical expenses and emergency medical evacuation, offers peace of mind, allowing travellers to focus on their adventures.

Flexibility in Trip Disruptions: Solo and adventure travel often involves changing plans on the fly.

While Singlife offers competitive coverage for travel delays or cancellations, its standout medical benefits ensure that health-related disruptions are managed promptly and efficiently.

My Review of Singlife Travel Insurance

While Singlife Travel Insurance Prestige offers a compelling package, it’s essential to remember that it’s not the only policy in the market.

Every traveller’s needs are unique, and what works for one might not be the best fit for another.

To ensure you’re making the most informed decision, take a moment to explore and compare various travel insurance options.

Dive into these comprehensive guides to get a clearer picture of what’s available:

You can find the perfect travel insurance tailored to your needs and adventures by comparing different policies.

So, after extensive research and comparison with other travel Insurance policies in Singapore, Singlife stands out as one of the best policies for International Business Travellers and Adventure enthusiasts.

With Singlife, your premiums are manageable, so you get value for your money, and paying for the premium does not break your bank account.

It is a competitive product and could be worth it in dire situations.

On the contrary, other insurers like Etiqa and Allianz might be more suitable plans for people with specific needs, such as pre-existing conditions.

Let’s now explore the Singlife Travel Insurance in depth:

Criteria For Singlife Travel Insurance

These requirements are essential for taking out a Singlife Travel Insurance policy.

- Have a valid NRIC or FIN

- Be at least 16 years old at the time of purchase (only required if you’re the applicant)

- Be taking a round-trip journey that begins and ends in Singapore

- Not travelling against the advice of a qualified medical practitioner

- Not travelling to obtain medical treatment

- Have purchased the policy before departing from Singapore.

Benefits Summary Cover & Limits

These detailed table illustrations provide an overview of the coverage limits across the Lite, Plus, and Prestige plans for the different sections and features of the Singlife Travel Insurance policy.

For Singlife Travel Insurance, these are the general summary benefits as a quick guide.

Premiums Rates

Here are the prices for both single trip (7 days) & annual plans for ASEAN and Global coverage for a 25-year-old Singaporean.

Singlife Travel Insurance Plan | Travel Lite | Travel Plus | Travel Prestige |

Price (ASEAN) | S$43.51 per week | S$61.67 per week | S$86.05 per week |

S$310 per year | S$440 per year | S$614 per week | |

Price (Global) | S$80.25 per week | S$116.94 per week | S$171.09 per week |

S$410 per year | S$598 per year | S$870 per year |

Prices are before any discounts.

Benefits Explained for Singlife Travel Insurance

General Exclusions

These exceptions apply to all sections of this policy unless otherwise specified. The insurer does not provide coverage for:

- War and Related Events

- Actions Linked to War or Terrorism

- Radioactivity

- Sonic Bangs

- Pollution or Contamination

- Wilful Acts or Negligence

- Unattended Property

- Pre-existing Medical Conditions

- Manual Work

- Sanction Limitation & Exclusion

There is not benefit if you are travelling through the following countries:

- Afghanistan

- Democratic Republic of Congo

- Iran

- Iraq

- Liberia

- Sudan, or

- Syria

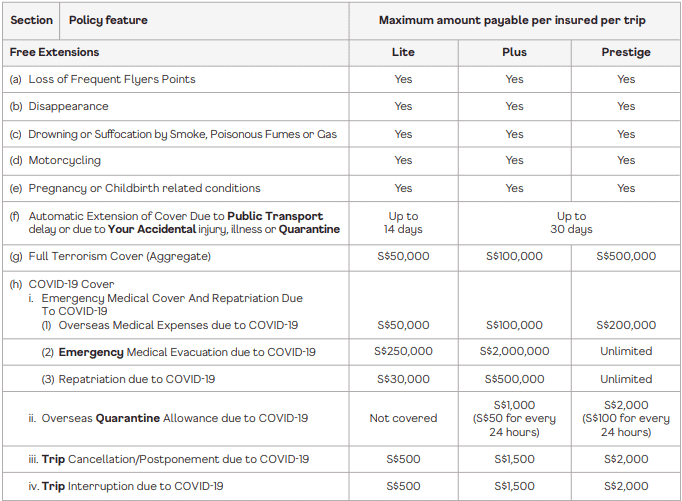

Free Extensions Under Singlife Travel Insurance

Here are a summed up points of the Free Extensions available under the Singlife Travel Insurance policy:

Loss of Frequent Flyer Points

Singlife will compensate the retail price of an airline ticket, Entertainment Cost, or booked accommodation purchased using Frequent Flyer Points in full if cancelled due to events covered under the policy. This Singlife Travel Insurance is applicable provided the loss of such points cannot be recovered from any other source.

Disappearance

In the event of the disappearance of the scheduled ship, aircraft, or train during the trip, leading to the inability to find the insured’s body within one year from the date of the accident, Singlife will consider the insured as legally dead. Compensation for Accidental death will be provided per the policy’s Schedule of compensation under Section 1a, with the condition that any beneficiary signs an undertaking to refund the amount if the insured is found alive.

Drowning or Suffocation by Smoke, Poisonous Fumes, or Gas

Singlife offers coverage under Section 1a for Accidental death, Permanent Total Disablement, or Accidental injury caused by drowning or suffocation by smoke, poisonous fumes, or gas, excluding events arising from the insured’s wilful or intentional act.

Motorcycling

The policy includes coverage for motorcycling, provided the insured wears a crash helmet, the driver holds a valid motorcycle license, and the insured is not engaged in motorcycling as a professional or in activities like speed or time trials, sprints, or racing of any kind. Note that personal liability cover for motorcycling is not included.

Pregnancy or Childbirth-related Conditions

Singlife will provide benefits under Section 12a, Section 14, or Section 15a if the insured is unfit to travel or continue with the trip due to pregnancy or childbirth-related conditions. These conditions must not be related to any Pre-Existing Medical Condition, and the expected delivery date should be no less than 12 weeks (or 16 weeks for a multiple pregnancy) before the planned return date.

Automatic Extension of Cover

The policy will automatically extend without additional premium if the insured cannot return home before the end of the Period of Insurance due to a delay in public transport (where the insured is not the cause of the delay) or due to accidental injury, illness, or quarantine. Singlife will continue to cover medical treatment under Section 4 – Emergency Medical Cover during this extended period if deemed medically necessary.

Full Terrorism Cover (Aggregate)

Singlife provides coverage up to the aggregate amount detailed in the policy for claims arising directly or indirectly from Terrorism.

Terrorism is defined comprehensively, including the use or threat of force and/or violence, harm or damage to life or property by various means for political, religious, ideological, or similar purposes.

How to Claim Singlife Travel Insurance

You should follow these steps to file a claim with Singlife Travel Insurance.

Register Your Account

- Register through the Singlife web portal ClaimConnect or download the Singlife app for iPhone or Android.

- ClaimConnect allows you to find the nearest panel clinic, file claims, and check claim status.

- Click on “Claims / Make a claim” to begin submitting.

- You must provide documents like medical bills, reports, or referral letters. Retain original documents for swift processing.

- Claims must be submitted within 30 days of the incident or as soon as possible.

- Providing and submitting documents like medical bills, reports, or referral letters are required to facilitate the claims process and avoid delays is important.

- Claim Review: Singlife will process claims within 10 to 14 working days of receiving all required documents. They will contact you for further clarification if needed.

Mail Original Documents

- You should indicate your policy number on the original documents for claims requiring reimbursements for upfront expenses (like medical receipts, purchase receipts, etc.).

- These documents should be mailed to Singlife Travel Insurance Claims, Singapore Life Ltd., 4 Shenton Way, #01-01 SGX Centre 2, Singapore 068807.

Acknowledgement and Further Communication

- Singlife will send an acknowledgement email within 3 working days after your claims submission.

- They will contact you within 30 working days if further information is needed.

- Once your claim is approved, the payout will be made via PayNow within 3 business days. Ensure your PayNow account is registered under your NRIC to receive the payment. If not, a physical cheque will be mailed within 14 business days.

- For more details or to view and submit claims online, visit the Merimen e-Claims portal.

Please note that it’s essential to have all required documents and complete relevant forms found in the form library on the Singlife website for successful claim processing.