Ever felt like your money just vanished into thin air?

I’ve been there too, trying to figure out where all my hard-earned cash went.

Budgeting can feel like a mystery, but it’s actually a powerful tool that can transform your financial life.

In this post, you’ll learn:

- Why budgeting is important

- Different types of budgeting methods

- How to choose the right budget system

With years of experience in personal finance and countless conversations with financial experts, I’ve gathered insights that can make budgeting simple and effective.

If you’re ready to take control of your finances and achieve your goals, keep reading.

You won’t want to miss out on these practical tips and strategies.

Let’s dive in!

Why is budgeting important?

Budgeting is crucial for managing your finances and achieving your goals.

Here’s why you should make it a priority:

It helps to manage your financial goals effectively

Budgeting is like a roadmap for your money.

By allocating funds to specific categories like savings, expenses, and investments, you can ensure every pound is working towards your financial goals.

Whether you’re saving for a house, planning a holiday, or building an emergency fund, a budget keeps you on track.

It allows you to see where your money goes and make adjustments as needed, ensuring you reach your goals efficiently.

It can assist with debt repayment

Dealing with debt can be overwhelming, but a budget can make it more manageable.

For example, you have a list of debts like this:

![]()

The above image is a tracker telling you what’s your loan balance, interest rate, and the progress of your debt.

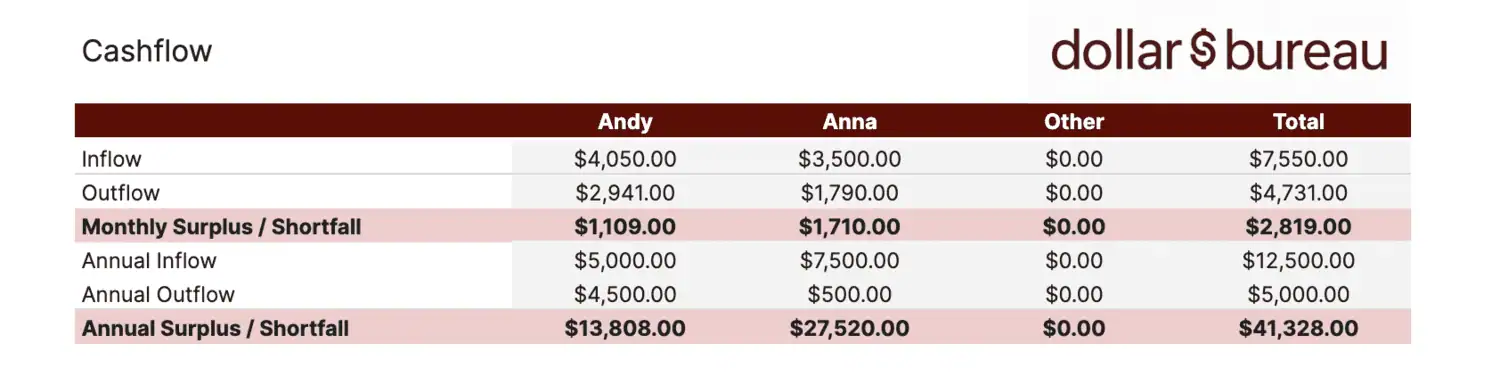

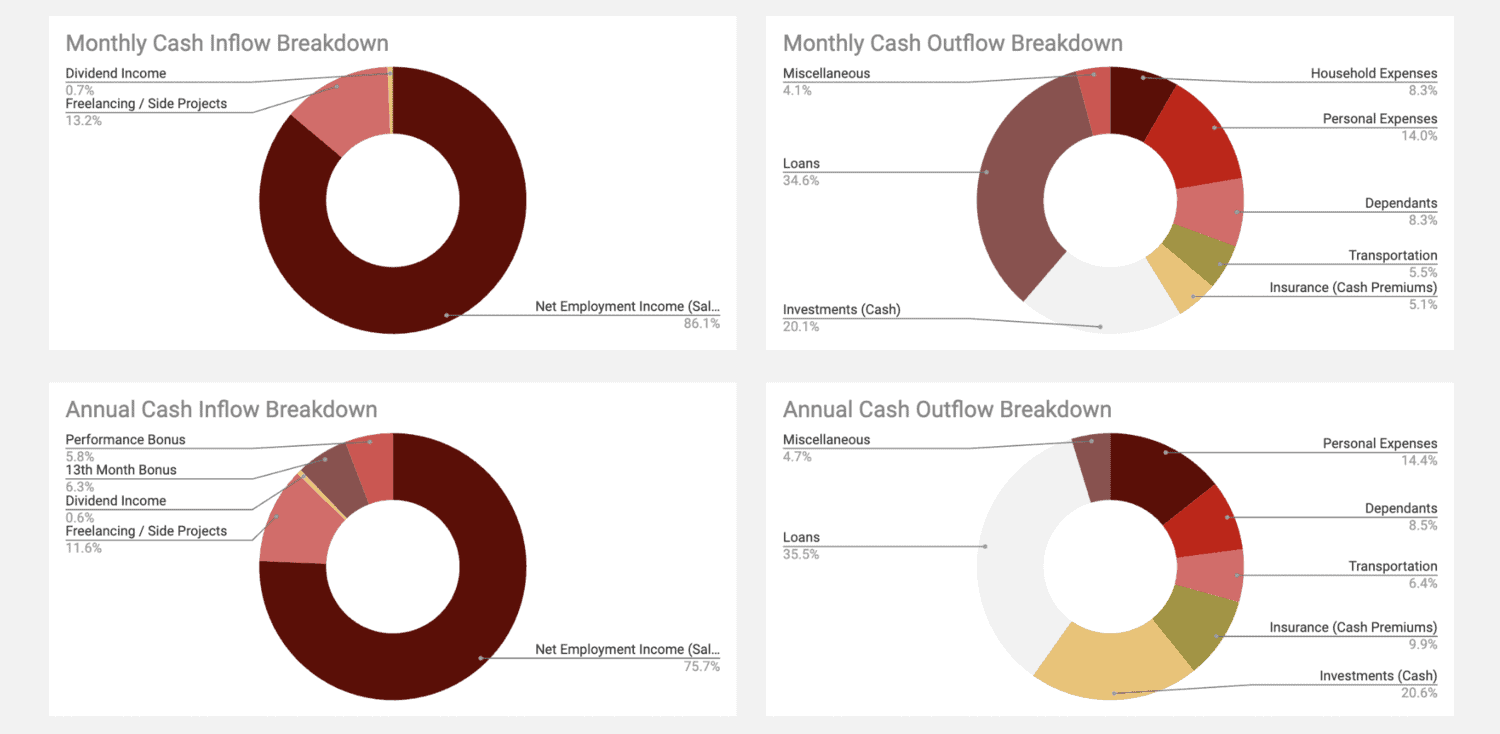

If you look at your own cashflow statement below, you’ll see that you might have a surplus in cash every single month:

With excess cash every month, you’re able to budget more for your loan repayments to make sure that you’re paying your debts on time, incurring lesser interest while paying less overall.

This is done by using proper budgeting techniques, identifying all your cash inflow and outflows.

By outlining all your income and expenses, you can identify areas where you can cut back and allocate more money towards debt repayment.

This structured approach helps you pay off debt faster and avoid additional interest charges.

For example, using the zero-based budgeting method (covered later) can ensure that every dollar has a purpose, prioritising debt repayment and reducing financial stress.

It can raise your credit score

A good budget can also improve your credit score.

When you consistently pay your bills on time and keep your credit card balances low, your credit score can increase.

A higher credit score can lead to better loan terms and lower interest rates, saving you money in the long run.

Budgeting helps you keep track of payment due dates and manage your expenses so you don’t miss any payments, directly contributing to a healthier credit score.

In short, budgeting is a powerful tool that provides clarity and control over your finances.

It not only helps you achieve your financial goals but also assists in managing debt and improving your credit score.

By incorporating budgeting into your routine, you set yourself up for a more secure and prosperous financial future.

Types of Budgeting Methods

Budgeting isn’t a one-size-fits-all approach.

Different methods work for different people based on their financial situations and goals.

Here are some popular budgeting methods:

The Zero-Based Budget

The zero-based budget requires you to allocate every dollar of your income to a specific expense, savings, or debt repayment.

The idea is that your income minus expenses equals zero.

This method forces you to be intentional with your money.

By giving every dollar a job, you can avoid unnecessary spending and ensure your finances align with your goals.

For example, if you earn $2,000 a month, you might allocate $800 for rent, $200 for groceries, $100 for utilities, $300 for savings, $200 for debt repayment, and so on until every pound is accounted for.

If you’re the type who likes to know where every single dollar of yours is going, this budgeting technique is for you.

The Pay-Yourself-First Budget

This method prioritises savings and debt repayment before anything else.

When you receive your income, you immediately set aside a portion for savings and debt payments.

The remaining amount is used for other expenses.

This approach ensures that your financial priorities are met first, helping you build a solid financial foundation and pay off debt more efficiently.

For instance, you might decide to save 20% of your income and allocate another 10% towards debt repayment, then budget the remaining 70% for living expenses.

The amount you allocate for each bucket depends on you, but this focuses on making sure you build your nest egg while reducing any liabilities you might have.

The Envelope System Budget

The envelope system budget involves planning your spending each month by categorising your expenses and placing the allocated cash into envelopes.

Once an envelope is empty, you cannot spend any more in that category.

This method is excellent for controlling spending and avoiding debt, as it limits you to the cash you have set aside.

For example, you might have envelopes for groceries, entertainment, dining out, and transportation.

When your dining out envelope is empty, it means no more meals out until the next month.

If you find that using cash is a little old school, you can still use this by taking note of how much you’ve spent for each “envelope”.

The 50/30/20 Budget

This is the most popular method that breaks down your expenses into 3 categories:

- Necessary expenses (50%)

- Discretionary expenses (30%)

- Savings and debt payments (20%)

By following the 50/30/20 rule, you can ensure that half of your income covers essentials like housing, utilities, and groceries.

30% can be spent on non-essentials like dining out, hobbies, and entertainment.

The remaining 20% is dedicated to savings and paying down debt.

By using a cashflow tracker like ours below, you can pinpoint what you’re spending on and categorise them accordingly to whats necessary, discretionary, and what’s for savings and debts.

Of course, if you don’t spend 50% of your income for your necessary expenses, you may choose to give yourself more budget for your discretionary expenses or even to your savings & debt repayments like what you see above.

This method offers a balanced approach to managing your finances, ensuring you’re not neglecting savings or overspending on luxuries.

The No-Budget Budget

The no-budget budget is a more relaxed approach.

Instead of tracking every expense, you focus on paying your fixed bills first and then freely spending the remaining money as you see fit.

This method works best for those who have a good handle on their finances and naturally spend less than they earn.

The key is to ensure that all essential expenses and savings goals are met before indulging in discretionary spending.

Each of these budgeting methods has its advantages and can be tailored to fit your unique financial situation.

By understanding and choosing the right method, you can take control of your finances and work towards your financial goals more effectively.

How to choose the right budgeting system?

Choosing the right budget system is essential for managing your finances effectively.

Here’s how you can find the best fit for your needs:

Figure out where you are and what you value

Start by assessing your current financial situation.

Take a look at your income, expenses, savings, and debts.

Understanding where you stand financially will help you determine what you need from a budgeting system.

Consider what you value most – is it paying off debt, saving for a big purchase, or simply managing day-to-day expenses?

Your values will guide you in selecting a budgeting method that aligns with your goals.

For instance, if debt repayment is a priority, the zero-based budget might be ideal since it ensures every pound is purposefully allocated.

Decide how much effort you’re willing to devote

Different budgeting methods require varying levels of effort and maintenance.

If you prefer a hands-on approach and enjoy tracking every expense, a detailed system like zero-based budgeting or the envelope system might suit you.

However, if you prefer something less time-consuming, the 50/30/20 budget offers a more relaxed yet structured approach.

Consider your lifestyle and how much time you can realistically commit to maintaining your budget.

Conclusion

Budgeting might seem daunting at first, but it’s a game-changer for managing your finances.

We’ve covered why budgeting is important, from managing your financial goals and assisting with debt repayment to boosting your credit score.

We explored different budgeting methods, like zero-based budgeting, the envelope system, and the 50/30/20 rule, to help you find one that suits your lifestyle.

We also discussed how to choose the right budget system by evaluating your financial situation and the effort you’re willing to put in.

If you’re serious about budgeting, using a tool like The Financial Toolkit will help you make better decisions while tracking your progress at the same time.

Remember, the key is to find a method that works for you and stick with it.