The Great Eastern GREAT Retire Income is a participating annuity plan that lets you enjoy your retirement years the way you like and with a stable monthly income.

As a participating policy, the plan allows you to accumulate cash through guaranteed and non-guaranteed bonuses.

You will enjoy multiple benefits such as the Loss of Independence (LOI) Income benefit, Presumptive Total and Permanent Disability (TPD), Death, and Terminal Illness.

Here, we comprehensively reviewed the Great Eastern Great Retire Income to determine if it’s the best policy to suit your needs.

Let’s jump straight in.

My Review of the Great Eastern GREAT Retire Income

The Great Eastern GREAT Retirement is an excellent retirement plan if you’re looking for guaranteed payouts – as this gives you the highest guaranteed payouts amongst all the annuities we’ve compared.

The GREAT Retire Income also offers capital savings, flexibility, and a stable income stream during your retirement, perfect for those looking for a retirement plan that’s stable and secure.

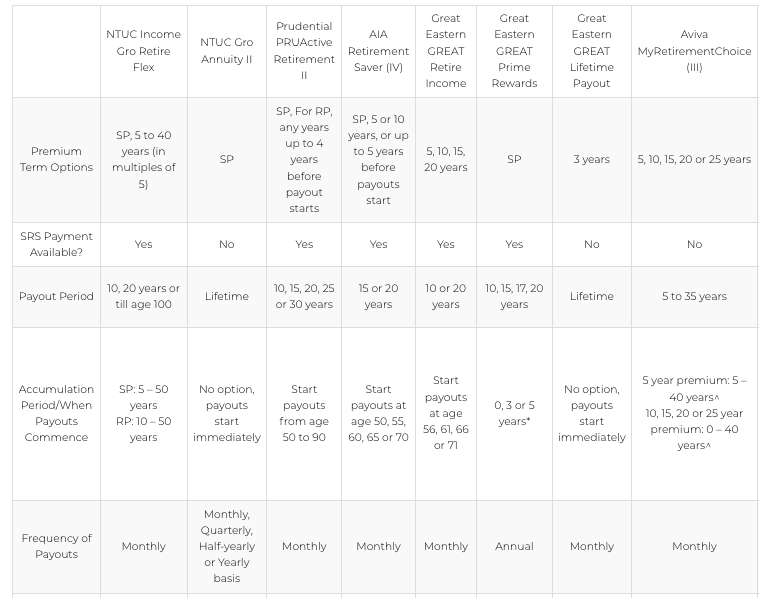

Comparison With Other Annuity Plans

We compare the Great Eastern GREAT Retire Income plan with other plans to better understand and help you choose the best option for your needs.

Subject to;

- Entry Age, premium payment term and accumulation period less than or equal to 80 ANB

- Additional payout plus basic monthly payout

- All policies payable in cash

As you can see, Great Eastern’s GREAT Retire Income has a decent choice of premium terms and payout periods.

It may not be the most flexible. However, it allows you to pay your premiums in cash or through SRS payment.

One unique advantage is that the policy offers an additional payout to help take care of your needs if you cannot perform 2 or more ADLs.

However, its disability coverage, in my opinion, isn’t as great as NTUC Income’s Gro Retire Flex.

Furthermore, it doesn’t offer incentives in case of job loss – something that NTUC Income’s Gro Retire Flex, Manulife’s RetireReady Plus III, and even AIA’s Retirement Saver IV.

Another drawback of this policy is that it doesn’t have optional add-on riders.

Therefore, there’s no option to beef up your protection or coverage. Also, there are no premium waivers if you get diagnosed with major illnesses like cancer.

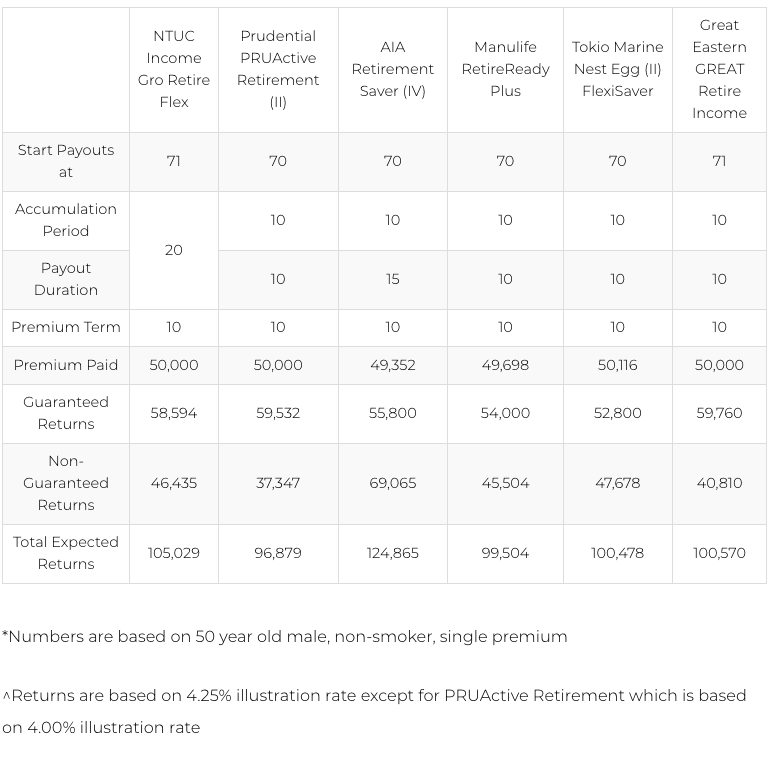

In addition, with an illustrated investment rate of return of 4.25%, it performs exceptionally well and can earn a high payout in the future – offering the highest guaranteed payouts among other plans.

On the whole, because of the multiple benefits that can match individuals’ different needs, I feel that it’s still a good plan to consider.

Furthermore, in our best retirement annuity plans comparison, the Great Eastern GREAT Retire Income was awarded as one of the best plans if you’re looking for guaranteed payouts.

Before choosing any annuity plan, it’s important to assess if there are any benefits and whether it will meet your retirement goals.

If you need help, contact a financial advisor who will help you make an informed decision.

Criteria

With this plan, you can choose your preferred retirement age, premium term, and how many months you’d want to receive the cash payouts.

- Retirement ages available: 56, 61, 66, or 71 years old

- Premium payment terms: 5, 10, 15, or 20 years

- Payout options: 10 to 20 years

Features

Great Eastern’s GREAT Retire Income has multiple features you can enjoy when signing up.

Premium Payment Options

You can select your preferred premium term ranging from 5, 10, 15, or 20 years, whichever appeals to you.

SRS payment options are also available, meaning you can pay with your Supplementary Retirement Scheme account.

Like other policies, in the case of regular premiums, you can pay monthly, quarterly, biannually, or yearly.

Payout Options

The monthly payouts start when you’re 56, 61, 66, or 71 years old, depending on your choice, with payout options between 10 to 20 years.

In addition, you can change your payout period at least 6 months prior to your first payout.

Monthly Cash Payouts And Non-Guaranteed Payouts

As mentioned earlier, you can choose when to retire and receive the guaranteed monthly cash payouts.

In addition, you can receive potential bonuses at your desired retirement age.

However, this is non-guaranteed as it depends on the illustrated investment rate of return (IIRR) and the actual fund performances.

Therefore, the bonus benefits may vary depending on the performance of the participating fund.

Loss of Independence (LOI) Income Benefit

Whenever you cannot perform 2 or more ADLs, you’ll receive 50% extra payouts of your monthly guaranteed income.

This amount is capped at S$2,500 monthly.

If you can’t perform at least 3 ADLs, you can get an LOI Income Benefit of up to 100% of the guaranteed monthly cash payouts.

However, the amount payable should not exceed S$5,000 per month.

ADLs are Activities of Daily Living, including washing, dressing, feeding, toileting, mobility, and transferring.

Capital Guarantee

The policy offers a capital guarantee as long as there are no alterations midway.

Bonus

This plan gives you guaranteed and non-guaranteed benefits. The guaranteed benefits are like rewards promised to you and will be given no matter how well the plan does.

Non-guaranteed benefits are rewards that depend on the performance of the participating fund.

There are 2 main types of bonuses for this plan:

Cash Bonus

Once a year, you will receive a cash bonus. Once declared, the cash bonus is guaranteed.

This bonus is divided into 12 monthly payments that you will receive over the course of a year.

Terminal bonus

This one-time bonus is not guaranteed and is paid only when your policy ends, either through surrender, maturity or death, whichever event first occurs.

Participating Fund Performance

The main goal of this plan is to provide insurance protection for you while also aiming to generate stable medium- to long-term returns.

The combination of guarantees and potential bonuses aims to give you a balanced approach that provides both protection and the opportunity for additional returns over time.

Asset Investment Mix

When you invest via a retirement or endowment plan, your payments are usually allocated to a participating fund.

This fund is responsible for investing in various assets like stocks, bonds, and other types of investments to achieve the highest possible return.

This investment strategy, known as diversification, aims to reduce risk by spreading out investments across different areas.

Table of strategic and actual asset mix for 2022 as of 31st December 2021:

| Type of Asset | Allocation Goals

(%) |

Actual Allocation

(%) |

| Bonds | 66 | 61 |

| Equities | 20 | 23 |

| Property | 10 | 8 |

| Cash | 0 | 5 |

| Loans and other assets | 4 | 3 |

| Total | 100% | 100% |

Investment Rate Of Return

As of December 2021, here is how the participating fund performed in the past:

Over a 5-year period, they have achieved an annualized return of 5.78% and over a 10-year period, an annualized return of 5.52%. These returns are quite impressive.

Compared to other insurance companies in Singapore, Great Eastern Life stands out with its geometric net investment returns.

This indicates that Great Eastern Life has been able to generate attractive returns on its investments.

Great Eastern Life’s track record suggests a strong performance in the market, making them a potentially reliable choice for investment purposes.

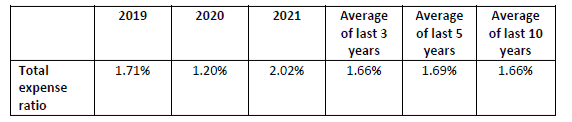

Past Total Expense Ratio

When investing in different mutual funds, it’s important to assess their total expense ratio carefully.

This ratio measures the amount of money a mutual fund spends concerning the assets under management.

These expenses include fees for consulting services, management costs, advertising expenses, taxes, and other administrative charges.

To help you make an informed decision, the following table shows expense ratios for Great Eastern Life:

Here’s the table you can use to compare the expense ratios of Great Eastern Life to other funds:

Protection

Death Benefit

Upon the demise of the insured, the beneficiaries will receive a payout of the higher of the following options as a single payment, minus any outstanding debts:

- 105% of the total regular annual premium paid, minus any survival benefits already paid out.

- The guaranteed surrender value.

In addition to these amounts, any bonuses that have been accumulated will also be included in the payout if applicable.

Terminal Illness Benefit

You receive the death benefit in a single lump sum if you’re diagnosed with an illness that may result in your demise within the next 12 months.

To be eligible, your diagnosis must be confirmed by a specialist and verified by a medical practitioner appointed by the insurer.

Total and Permanent Disability (TPD) Benefit

If the person insured under the policy experiences total and permanent disability before the policy anniversary on which they reach the chosen retirement age, they will receive a single lump sum death benefit.

However, once the policy anniversary on which the selected retirement age is reached, the TPD benefit will no longer be applicable.

There are 2 types of TPD:

Presumptive TPD

Presumptive total and permanent disability (TPD) is a condition where you become completely and permanently incapacitated in one of the following:

- You lose eyesight in both eyes.

- You lose the use of your 2 limbs, either at or above the wrist or ankle.

- You lose the eyesight in one eye and the use of one limb at or above the ankle or wrist.

It applies throughout the entire policy term, meaning you’ll be covered for this type of disability as long as your policy is active.

Non-presumptive TPD

With this policy, if you become disabled and unable to work due to an injury or illness, you may qualify for TPD coverage under your policy.

For those above 15, you’ll be considered TPD once your disability completely and permanently prevents you from working and earning any income or profit now and in the future.

For those aged 15 and below, you’ll be considered TPD when you are completely and permanently confined to your home, a hospital, or another care facility for at least 6 consecutive months, and you require constant medical attention during this time.

The Great Eastern GREAT Retire Income guarantees non-guaranteed and regular income in your golden years. The table below summarises the type of benefits to expect with this policy.

Summary of the GREAT Retire Income

| Cash and Cash Withdrawal Benefits | |

| Cash value | Available |

| Cash withdrawal benefits: | Available |

| Health and Insurance Coverage | |

| Death | Available |

| Total Permanent Disability | Available |

| Terminal Illness | Available |

| Critical Illness: | Not available |

| Early Critical Illness: | Not available |

| Health and Insurance Coverage Multiplier | |

| Death | Not available |

| Total Permanent Disability | Not available |

| Terminal Illness | Not available |

| Critical Illness | Not available |

| Early Critical Illness: | Not available |

| Optional Add-on Riders | Not available |

| Additional Features and Benefits | LOI Income Benefit

Monthly cash payouts Non-guaranteed benefits Capital guarantee |

An Illustration of How Great Eastern’s GREAT Retire Income Works

To understand how the policy works, we shall look at an illustration.

Peter is a 35-year-old employed male who intends to retire at 66. He chooses the Great Retire Income policy and pays S$400 per month.

He then chooses a 5-year premium term. Subsequently, the premium ends at 40 years.

Here we explore two scenarios where he chooses a 10 or 20 years income period.

Example 1 (10-year income period)

If Peter chooses an income period of 10 years, he will receive guaranteed and non-guaranteed retirement income of S$731 each month when he retires at 66 years.

At 76 years, the policy will end; by then, he’ll have received retirement benefits totalling $87,770.

In this case, the total payouts received against the total annual premiums paid are 3.65X.

Example 2 (20-year income period)

If Peter chooses an income period of 20 years, he will receive guaranteed and non-guaranteed retirement income of S$438 every month upon retirement at 66 years.

Subsequently, the policy will end when he is 86 years old.

At this time, he’ll have received total retirement benefits totalling $105,200, equivalent to 4.38X total payments received against total annual premiums paid.

If Peter loses the ability to perform at least 2 ADLs during the income period, he will be paid an extra LOI Income benefit. The amount payable is 50% of the guaranteed monthly cash payout.

Note that the calculations are based on an Illustration Rate of Return (IIRR) of 4.25% p.a for the participating fund.

Likewise, the payouts comprise both guaranteed monthly income and non-guaranteed bonuses.